Business

Facebook - A Case Study - Part 2

Facebook - Part 2: Facebook Financials Analysis

This is the second of my three-part Facebook research series. It provides some background numbers on how the company is doing financially based on figures on their public website at the 3rd quarter of 2016. These information would eventually build up to my market strategy analysis at part 3.

Overview

Facebook is currently the largest social networking platform in the world that has been experiencing significant growth and value. In the latest Fortune 500 report, Facebook has been listed for 4 years, and has increased its ranking from 242 to its current ranking at 157. It is also ranked number 3 in the 100 fastest growing companies

Background

Facebook was founded in February 2004, and it went public on May 2012

On February 2012 when Facebook filed its S-1 Form, the

company was primarily in the display-advertising business with a net profit of

$1 billion in 2011 from a total revenue of $3.7 billion (Safdar, 2013) . It is interesting

to note that when Facebook went for IPO, its prices were at record value of $38

a share, which equates to around $104 billion market valuation (Wall Street

Journal, 2012) .

This, however, did not last long as it was noted that with more users moving

from desktop to mobile platforms, the initial projected revenue was

misrepresented. This led to a revised S-1 where Facebook released to the public

that mobile ads presented an ongoing challenge for the firm. That impacted

investor’s confidence, and prices plummeted ever since. It took almost a year

later in July 2013 for the prices to return to the initial price after Facebook

released more features like Facebook Exchange in bids to have more targeted

advertising to fulfill advertising demand (An, 2014) . Much have

progressed since. Facebook picked up on this area and have new solutions like

Dynamic Ads and Custom Audiences that have mobile at their core and are

delivering excellent results for the businesses. Developers can also access

Facebook APIs to innovate and build great advertisement experiences for their

brands and customers. These new solutions work so well in revenue generating

that Facebook prices have been increasing ever since, and Facebook recently

announce to decommission its old advertising solution, Facebook exchange, in November

2016 this year make way for new advertising solutions (Marvin, 2016) .

Financial

Situation – Rapid Growth

To understand Facebook’s current financial situation,

I started by looking at the latest financial reports in Facebook’s official investor’s

website (Facebook, 2016) . My overall analysis

is that Facebook is currently at a good financial situation and the information

below will elaborate this finding further.

From the Assets category in the Balance Sheet, we can

tell that Facebook’s total asset value has been constantly increasing over

time, reaching its current peak at $55.74 billion. Also, with some calculation,

the rate of increase is generally increasing over time too (i.e. from 5.17% in

early 2015 to 7.04% in 2016). It is also interesting to note that most of the

increase is due to marketable securities from current assets. Goodwill also

takes up a significant portion of Facebook’s assets. Other assets like property

and equipment takes up a much smaller amount in comparison. These means

Facebook’s key assets are less physical in nature, and are increasingly on investments

in marketable securities that can be easily converted back to cash later if the

need arises.

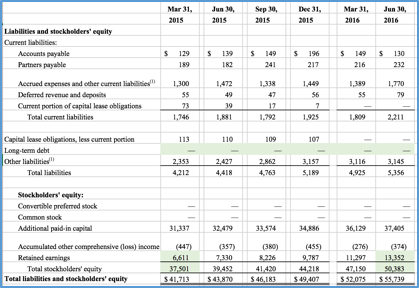

Next, looking at Facebook’s Total Liability and Total Stakeholder’s Equity, we can tell that the company has cleared all of its long term debts for a period of time, and is highly profitable considering the continuous increase in retained earnings from around $6 .6billion in 2015 to more than two times the original amount at $13.35 billion at the last quarter. This increases the total stockholder’s equity from $37.5 billion in 2015 to the current $50.4 billion today. This is a good sign because instead of having debt in the liabilities section to pay others, money is in its stockholder’s pocket, ready to continue to invest back into the company for future growth.

Next, moving on to the income statements, Facebook’s

current revenue is at $6.44 billion. Comparing the rate of increase in revenue

($6,436-$3,543 =$2,893) with total costs and expenses ($3,690-$2,610=$1,080), the company is generally making money faster than it is spending. The chart below further elaborates Facebook’s

revenue growth in comparison with the Year-Over-Year growth. We can see that

the trend is positive.

This is useful information because though most of Facebook’s revenue is from two categories, “Advertising” and “Payments and Other Fees”, and we can see from the chart that “Advertising” takes up a significant larger portion of the pie (i.e. 96.94% in Q2’16 ). Considering the attractiveness of a platform for advertisers is its effective outreach, the increase in active users would have a positive corelation with the amount of revenue from advertising.

Finally, it is also

interesting to consider the spending power of the users that are on Facebook’s

platform. For example, though the number of monthly active users in US &

Canada is smaller (226 million) in comparison to the rest of the world (556

million), the revenue is $3,212 million in comparison to $614 million. In other

words, every user in USA & Canada is generating $13.74/user, but the number

is significantly smaller at $1.12/user in the Rest of the World.

Financial Stability

Though most Software-as-a-service companies can be

analyzed with the Cost of Customer Acquisition (CAC) in comparison to the

monetization in Life Time Value (LTV) (Skok, 2014) ,

the formula for the Magic number does not fully apply for Facebook. This is

probably because Facebook does not follow a subscription model, and does not seem

to use Sales and Marketing expenditure as a key avenue to acquire customers.

Furthermore, the lifetime of its customers can last for years, as long as the

platform remains attractive to them.

Also, Facebook has a more interesting way to acquire customers. They do it through acquisitions and this move allows the company to not only purchase users, it also allows Facebook to acquire talents as employees in their firm. Some of the more famous acquisitions include purchasing Instagram for $1 billion in 2012

Among these acquisitions, the most interesting one is with Whatsapp. At the time of acquisition, WhatsApp is an ad-free mobile application that is free to use, with subscription kicking in after the first year. The messaging service which reached 400 million active users in December, generated less than 3 cents in revenue per user. Though that sums up to around $10.2million in total revenue, its net loss was $138.1 million in 2013. Despite these losses, Facebook’s $21.8 billion acquisition equates to paying for $55 per user

When comparing Facebook to its competitors, we can

look at the net profit margins (Analysis, 2016) . From the table below, we can see that Facebook

is generally doing well other than the year it IPO in 2012.

To analyze Facebook’s financial stability, investors would be interested in the ROIC (Return of Invested Capital), ROA (Return of Assets) and Return of Equity (ROE). The tables below generally show an upward trend.

This upward trend is also further supported by the Earnings per Share (EPS) figures from NASDAQ

Claims of effective advertising on Facebook and

Instagram is backed up by examples. For example, Lighting Etc., a

third-generation family-owned business, used Facebook and Instagram ads to

drive in-store sales. They targeted 25-45-year-old homeowners interested in

interior design, living within 35 miles of their showroom in Fort Worth, Texas.

It was striking to them that being on Facebook meant they could reach over

300,000 people even with such specific targeting. They have seen a 40% increase

in revenue in 2016.

Though these advertisement methods prove to be

working, the only word of caution is that Facebook pages is currently already

filled with “Ad Load”. In other words, it has currently crammed the newsfeed of

its users to a point that it thinks it can fit without turning users off (D'Onfro, 2016) . Facebook needs to

figure how to increase revenue from advertisements without increasing the

quantity of advertisements appearing for its users. Also, more may need to be

done to figure how to monetize people in other regions of the world that has

less spending power. Other than this, the company’s general outlook looks great

for investors considering it is still continuously growing its user base and

engaging them to be active users, and balancing the expenses out by increasing

its revenue through effective advertising.

Conclusion

Therefore, in summary, for Facebook’s current

financial situation, its large volume of user generated data and advertisers

are the biggest contributors to its financial health. With over 1.7 billion

users, Facebook is able to continuously distribute advertisements on its two

main platforms on Desktop and Mobile, making an average of $3.82 per user

worldwide. The future outlook looks good as well for Facebook as it

continuously seeks ways to increase its user base and address it with effective

targeted advertising. To continue to stay attractive for investors, Facebook

will need to continuously seek ways to retain the number of active users, increase

the value per user not only in developed countries, but also in developing

countries, while balancing the amount of advertisements shown, ensuring that it

does not turn their users off.

References

Crunchbase. (2016, October). Crunchbase. Retrieved from Crunchbase: https://www.crunchbase.com/organization/facebook

Statista. (2016, October). Statista. Retrieved from Statista: https://www.statista.com/statistics/264810/number-of-monthly-active-facebook-users-worldwide/

Wall Street Journal, S. R. (2012, May 17). Facebook Prices IPO at Record Value. The Wall Street Journal.

Safdar, K. (2013, May 20). The Atlantic. Retrieved from The atlantic: http://www.theatlantic.com/business/archive/2013/05/facebook-one-year-later-what-really-happened-in-the-biggest-ipo-flop-ever/275987/

An, Z. Y. (2014, July 29). Lei Phone Net. Retrieved from Lei Phone Net: http://www.leiphone.com/news/201406/facebook-nixi-wall-street.html

Marvin, G. (2016, May 25). Marketing Land. Retrieved from Marketing Land: http://marketingland.com/facebook-sunset-fbx-desktop-retargeting-favor-mobile-capabilities-178703

Facebook. (2016, October). Facebook. Retrieved from Facebook: https://investor.fb.com/financials/?section=quarterlyearnings

Fortune500. (2016, October). Fortune 500. Retrieved from Fortune 500: http://beta.fortune.com/fortune500/facebook-157

Skok, D. (2014). For Entrepreneurs. Retrieved from For Entrepreneurs From David Skok: http://www.forentrepreneurs.com/customer-acquisition-monetization/

Deutsch, A. L. (2015, March 25). Investopedia. Retrieved from Investopedia: http://www.investopedia.com/articles/investing/032515/whatsapp-best-facebook-purchase-ever.asp

Dredge, S. (2014, July 22). The Guardian. Retrieved from The Guardian: https://www.theguardian.com/technology/2014/jul/22/facebook-oculus-rift-acquisition-virtual-reality

Frier, S. (2014, October 28). Bloomberg Technology. Retrieved from Bloomberg Technology: https://www.bloomberg.com/news/articles/2014-10-28/facebook-s-22-billion-whatsapp-deal-buys-10-million-in-sales

Gelles, D. (2014, February 20). Deal Book. Retrieved from Deal Book: http://dealbook.nytimes.com/2014/02/20/for-facebook-its-users-first-and-profits-later/?_r=1

D'Onfro, J. (2016, July 27). Business Insider. Retrieved from Business Insider: http://www.businessinsider.com/facebook-ad-loads-less-important-for-growth-2016-7

Analysis, S. (2016, October). Stock Analysis on Net. Retrieved from Stock Analysis on Net: https://www.stock-analysis-on.net/NASDAQ/Company/Facebook-Inc/Long-Term-Trends/Net-Profit-Margin#Comparison-to-Competitors

Focus, G. (2016, October). Guru Focus. Retrieved from Guru Focus: http://www.gurufocus.com/term/ROC/FB/Return-on-Capital/Facebook-Inc

Nasdaq. (2016, October). Nasdaq. Retrieved from Nasdaq: http://www.nasdaq.com/symbol/fb/eps-forecast

Main image: http://www.makeeasymoney365.com/wp-content/uploads/2012/04/Facebook-IPO.jpg

No comments